- Over a third of new car loans now stretch beyond six years.

- A growing share of buyers are signing 85-month terms.

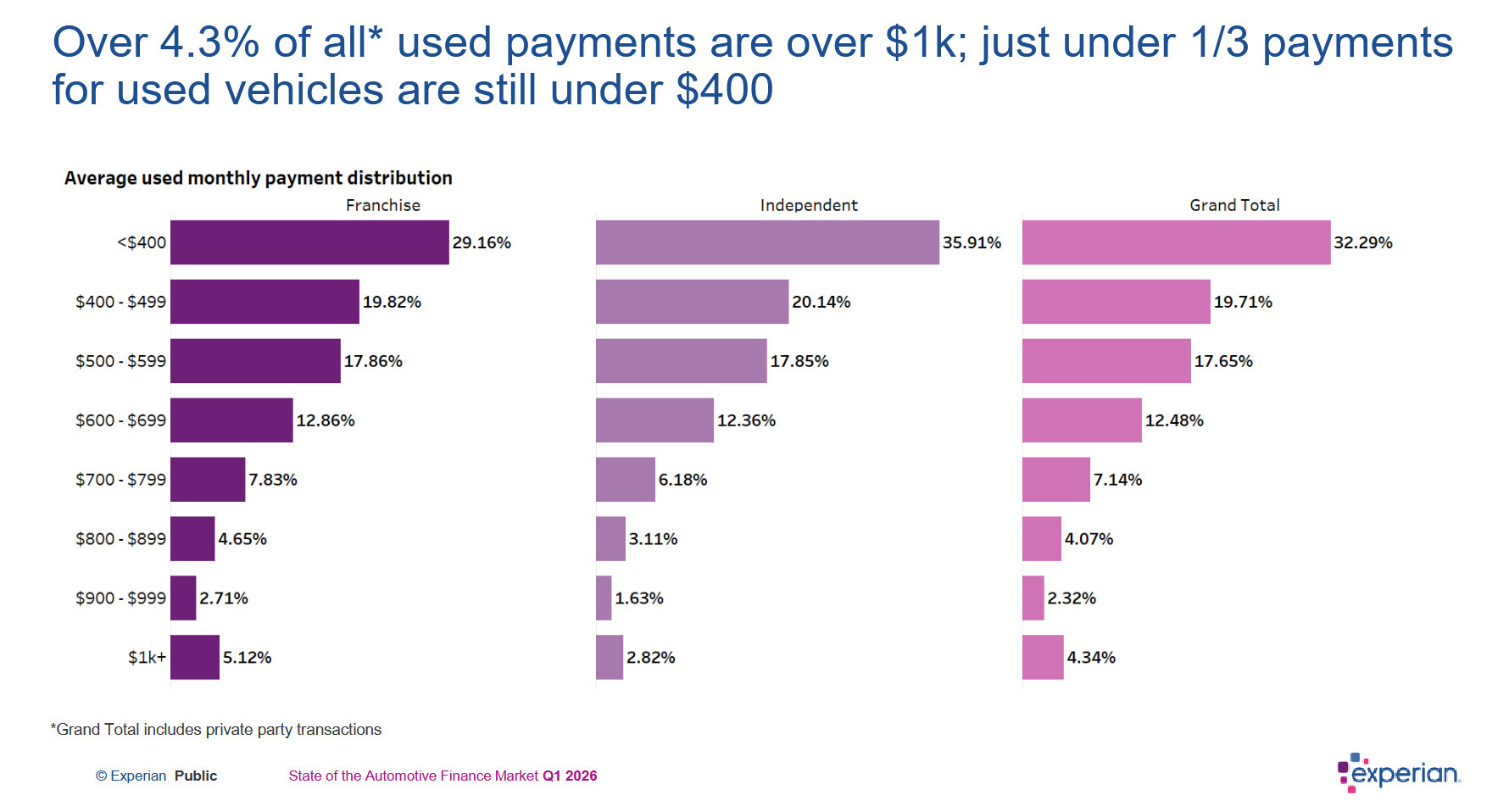

- Most $1,000 a month car payments aren’t for luxury models.

Americans are borrowing more and stretching the payback further just to park something new in the driveway, and the result is a swelling number of buyers handing over more than $1,000 a month. It’s a sober reminder of just how easy it is to become swamped in debt while trying to pay off a vehicle loan.

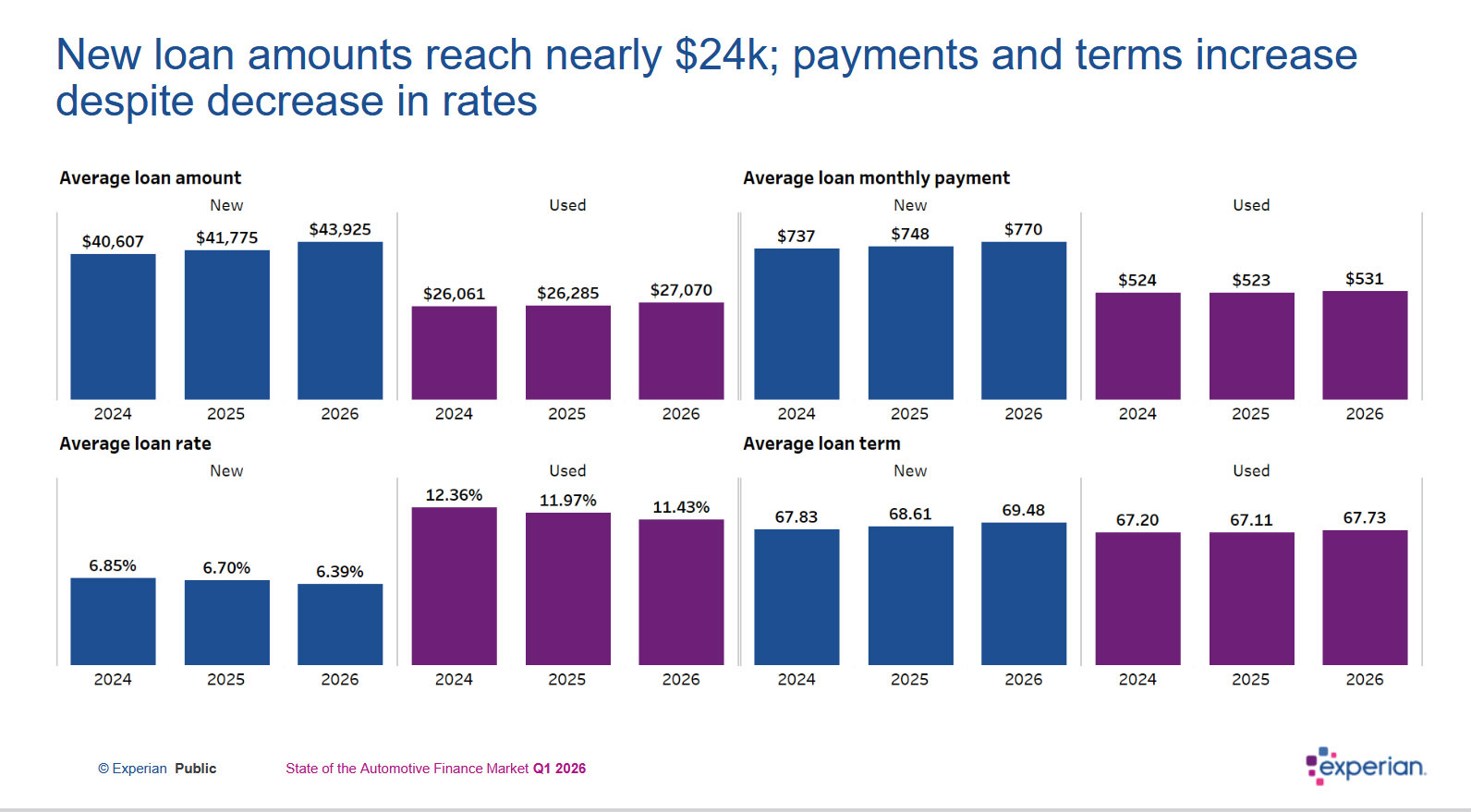

A new analysis from Experian Automotive shows the share of new vehicles financed over terms longer than six years climbed to 35.6 percent in the first quarter, up from 30.8 percent a year earlier. More striking still, 3.3 percent of new-car buyers are now signing loans that run 85 months or more, up from 2.9 percent.

Read: More Than Half Of US Car Buyers Are Underwater, Top Lender Isn’t Worried

The same pattern appears in the used market, where loans longer than six years rose from 28.6% to 31.5%, while those exceeding 85 months increased from 1.3% to 1.4%. Experian’s Melinda Zabritski said affordability remains a major factor in financing decisions, with more consumers turning to longer-term loans to keep monthly payments manageable.

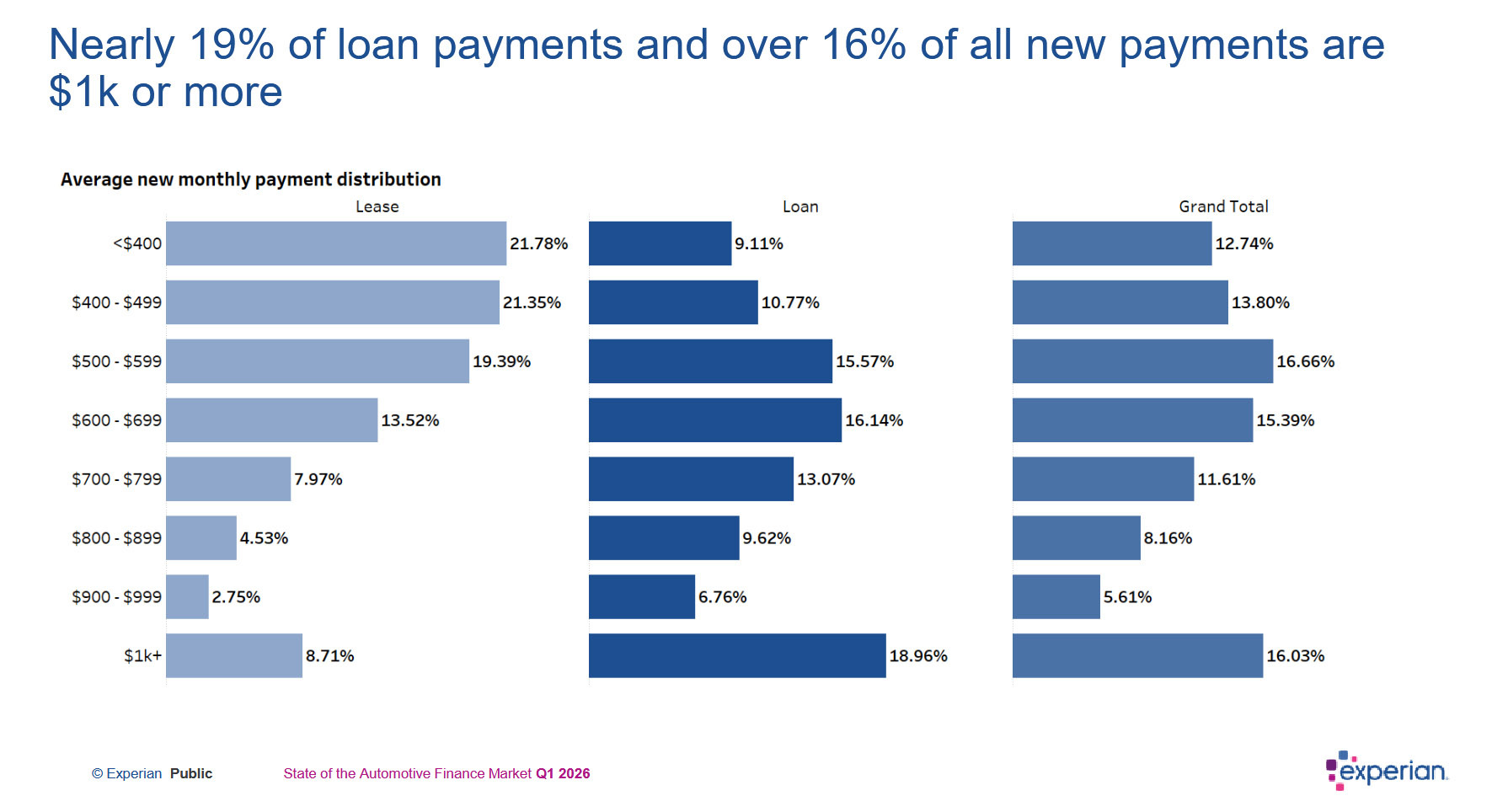

The numbers are telling. In the first quarter of 2026, the average new-vehicle loan climbed $2,150 year-over-year to $43,925, pushing the typical monthly payment from $748 to $770. Predictably, more and more buyers are now paying back over $1,000 a month. Not everyone is in that boat, though, with nearly 20% of new loans still landing below $500 a month.

Drowning In Repayments

The analysis of more than 5 million open car loans and leases reveals that almost 19% of those for new vehicles exceed $1,000 per month, rising from around 17.4% this time last year. This isn’t because car buyers are opting for higher-end models, either. In fact, of those loans with monthly payments exceeding $1,000, roughly 74% are for non-luxury models, often including expensive pickups like the Chevrolet Silverado 1500, Ram 1500, and Ford F-150.

As reported by CNBC, just 5.4 percent of new vehicle loans had monthly payments exceeding $1,000 just five years ago. However, as new vehicle prices have soared after the Covid-19 pandemic and semiconductor shortages, so too have loan repayments.

It’s not just new vehicles that are impacted. The average loan amount for a used car has also increased $785 year-over-year to $27,070 through the first quarter. In addition, the average monthly payment has risen from $523 to $531.

Experian also found that the average new-car loan term reached 69.5 months, while used-car loans averaged 67.7 months. Separately, consumers who refinanced auto loans reduced their interest rates by an average of 2.2 percentage points and lowered monthly payments by $81.